DEFINING RISK ECONOMICS AS A SOLUTION TO THE EMU & THE GLOBAL MONETARY SYSTEM SHORTCOMINGS

Risk Economics is a novel branch of Applied Economics, term first coined in 1996 by myself in my seminal work ” Risk Economics: Innovative and Scientific Approaches to the Application of Risk Management”, a study undertaken from private research spanning more than a decade. The work is the major inspiration for the setting up of Lyscale Riskgrade as a viable professional service entity with a financial engineering firm dimension doubled with an Investment Banking concern providing cutting edge financial risk instruments and vehicles for Risk Products and Services.

Risk Economics is the Economic Management of Risk. Risk is an undesirable commodity that occurs by virtue of all cardinal states.

The objective of Risk Economics oscillates around the reduction and elimination of all types of risks facing businesses and other organizations using scientific approach to the problem of dealing, avoiding, reducing, and transferring risks. The scientific predisposition of Risk Economics stems from and involves the application of the scientific method to the process of managing risks and the use of the decision theory in solving risk management problems. Fundamentally, risk management is a problem in decision making as explicated grandly by Professor Emmett J. Vaughan at the University of Iowa, USA. According to his wise perception, Risk Management is therefore more specifically a problem of decision making under conditions of uncertainty. Once a problem is identified, related information is analyzed and evaluated. Alternative solutions are identified, and the one with the greatest potential for success is selected. So were it not for the advances in scientific decision making, it seems doubtful that risk management would have evolved as a discipline.

THE PROBLEMATIC DIMENSION OF RISK ECONOMICS AND ITS MANAGEMENT

Risk has a temporal perspective for it has existed throughout immemorial times to this day. Exposure to misfortune and adversity brought enhanced gradualist efforts from humans to deal with risks of all sorts. Our ancestors’ instinct of survival can be amalgamated to a situation of observed practices tending to prevent the occurrence of risky events, which, most of the time coincide with extinction. Our continued existence is testimony to the success of our ancestors in managing risks. Today the apprehension that our hazardous environmental derivatives foster via climate change, hurricanes, drought and other predictable calamities equate to the perils that threatened primitive man shivering in the cold, suffering pangs of hunger, and hunted by savage beasts or stronger opponents.

Managing risk is corollary to sound assessment of the environment in which exposure evolves. Time frame consideration is pivotal to sound prediction of adversity. Outside temporal dispositions, risks adopt exponential tendencies most of the time with little influence on tolerance. This obsolescence of risk occurrence is reflected in many fields and industries. It does not necessarily imply an actual adversity outside perceptive prejudices. Decision making under Uncertainty dictates that the expected value model cannot be used and a different approach is desirable as a condition sine qua non, sufficient and necessary if all things are to be viewed as equals, ceteris paribus. Using our methodology, the minimum payoff for each choice is to maximise the minimum possible profits in the spirit of the maximum strategy. When decision making process is faced with problems such as those in which payoffs en relation to costs are to be minimised, the maximum approach is reversed, in that the decision maker lists the costs associated with each decision. In tuned with the Economics Analytics of our deployment, our recommended decision takes the whole ambivalence-discount of the Risk Spectra clearly isolated within Lyscale Riskgrade Master Layout and then responds to the minimum of the maximum costs, giving rise to the term LYSCALE MINIMAX. The beauty behind Risk Economics as pioneering by Lyscale Riskgrade is that its renderings are solidly subtracted from the erratic judgemental approaches exercised since now and by ricochet, we bring the scientific dimension of Risk Measure Precision to astronomic heights. Even though no system based on empirical observation and Cartesian argumentations is infallible, we proud ourselves with the infinitesimal margin of errors we normally encounter in assessing identified and isolated risks of all natures. An element of nature is always at hand to disrupt our forecasting and predictions but such element is effectively accounted for in the classes of Systemic Risk in Interactive Markets (SRIM) and in our Inherent Risk Suite.

EVOLUTION OF ORGANIZATIONAL RISKS

Organizational Risks evolve like any other phenomena characterized by its dynamic scope and stance. Like such phenomena, risks are no different. Organizational risks follow a well-defined pattern of occurrence and tend to be jugulated by the sheer response of man-made solutions in temporal and space contexts. When risks occur, they are addressed and solutions are put in place to prevent them from happening in the future. This approach of self-defence induces a dynamic effect that in turn triggers dimensional moral hazards and asymmetric information flaws exploited by organizational agents. Lyscale Riskgrade has put in place a mechanism addressing this aspect of recurrence in a scientific setting. Evolution imperatives apply a set of tools designed specifically in order to fine-tune actions of adversity induced by detrimental behaviour of organizational agents. This takes into account realms of deployment unforeseen in the past.

RISKS IN A GLOBAL GROWTH CONTEXT

Our theory of Global Growth is comprehensively dealt with within the GLOBAL MACROECONOMIC OBSERVATION SYSTEM (GMOS) PLATFORM with pioneering deployment of a set of tools acting like Indexes of measures aiming to eliminate dysfunctional and discrepancies observed in the assessment and prevention of risk occurrence. The set, although, globalist in outlook, embeds sophisticated financial engineering rationales disseminated at precise micro-levels.

RISK IN THE MODERN BUSINESS ENVIRONMENT

In the business world, risks are sub-divided into categories ranging from financial, operational, computational and credit compartments with specialised fields of applications and a varying degree of shortcomings. Many Experts in Risk tend to assimilate Risk as a concept to virtually everything they do not comprehend. This stance is far from the reality. Risk in the Business Environment is a science with real variables and specifics, properly defined, isolated and dealt with. It involves most of the times, the measurement and management of these risks, the valuation and hedging of products related to risk instruments, and the promotion of greater understanding in the area of risk theory and practice. Research in the field of business related risks is extensive, comprehensive with more or less headways made in recent years. Lyscale Riskgrade is working hard to provide a greater access to these highly technical expertises, not widely understood and accessible to the wider audiences, by providing the layman-connectivity gap filling approach with technical jargon translated into simple expressions.

RISK AS A CONCEPT

The abundance of definitions affiliated to the concept of risk provides proof if any that the matter is of pivotal importance in today’s society. Virtually, every field of knowledge has its own specialized terminology, and terms that have very simple meanings in everyday usage. Economists, statisticians, decision-theorists, insurance theorists and many other self-proclaimed experts use different definitions when it comes to Risk.

Our definition of risk is simple: “a condition of the real world in which there is an exposure to adversity. A condition in which there is a possibility of an adverse deviation from a desired outcome that is expected or hoped for.” This definition encompasses various terms and notions including (1) the chance of loss; (2) the possibility of loss; (3) uncertainty; (4) the dispersion of actual from expected results; and (5) the probability of any outcome different from the one expected.

Risk has two components:

1. uncertainty, and

2. Exposure.

If either is not present, there is no risk.

The development of Lyscale Riskgrade’s scientific measure of risk in virtually every asset and liability class conceivable, one need to explore, in turn, some fundamental mathematical notions and definitions. Although, we endeavour to bring our mathematical formulation to a strict minimum so as to enable everyone to grasp our demonstrative reasoning, it is also true that a minimum mastery in pure and applied mathematics is essential for a comprehensive understanding of what it is all about.

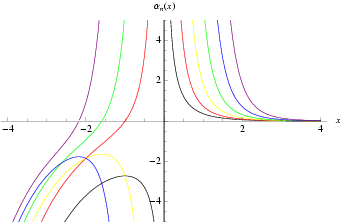

First, we explore the notion of a hypothetical Risk Exposure Line (REL) in a Cartesian setting. We denote Pn(S/R) as the Gradual Evaluative Level of Magnitudes by which the Exposure Element of Risk (S/R) as a combination of Exposure and Uncertainty evolves. S/R, on the ordinate level, expresses the cumulative sums of Economic Exposure (Money) of Risk without the Uncertainty element in its composition. The scientific premises by which we reached the rationale in isolating the Uncertainty element of Risk for the first time in the history of the subject rely surprisingly on obvious logical drawings: in general and empirically proven is the fact that pair wise loss given default (LGD) correlation is found to be small (5.9% for large corporate obligors that we comprehensively researched over the past ten years with respect to the Lyscale Riskgrade’s Risk Audit for Entities, Global 500 section). Another observation arises from the following perspective: since pair wise correlation is small between the Exposure Element and the Uncertainty element of Risk, economic capital is found to be more sensitive to changes in idiosyncratic probability default/loss given default (PD/LDG) correlation than those in systematic PD/LGD. As shown on the figure below, it is clear that at Unity (i.e. point 1), the Uncertainty Element of Risk adopts a declining tendency while the Exposure Element of Risk increases and starts declining with Risk Magnitude increasing. By the time Risk Magnitude approximates the level 2 on the Lyscale Riskgrade System, Risk Uncertainty declines precedence over the Exposure Element and both start evolving at very negligible level, nearing zero. Risk Exposure Line

Picking as shown by the graph above

UNCERTAINTY AT THE PERIPHERY OF RISK

Uncertainty is a state of mind characterized by doubt, based on the lack of knowledge about what will or will not happen in the future. This amounts to a psychological reaction to the absence of knowledge about the future in relation to a given problem. So the existence of Risk, which is a condition or combination of circumstances in which there is a possibility of loss, creates uncertainty on the part of individuals when that risk is recognised. Therefore, uncertainty is a peripheral perception inducing negation over the positive outcome of something contingent to fluctuation or to change. Uncertainty exists only when risk exists. However, risk can be isolated and identified without the prevalence of uncertainty.

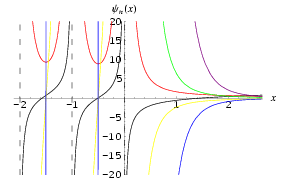

Second, we explore the notion of the Alpha Function as explicated in the graph below.

Alpha Function

In finance, alpha is a financial measure giving the difference between a fund’s actual return and its expected level of performance, given its level of risk (as measured by beta). A positive alpha indicates that a fund has performed better than expected based on its beta, whereas a negative alpha indicates poorer performance. This notion of an Alpha Function confirms a solid basis of deploying Financial Risk in that it enables practical approximations in terms of providing mirroring Betas in the Capital and Money Markets via Special Financial Instrument Computation. The modelling predisposition using Alpha Function provides accuracy in terms of realistic assumptions whereby every conceivable postulate is self-assessed for realistic adoption. The vast morass of Financial Statistics Indicators, most of them meaning approximately nothing and entirely useless, is mind-boggling if one truly wants to make sense of them all or in isolation. Alpha Function rationale, used in a consistent manner, therefore provides a scientific way of making realistic approximations in all fields of Risk Economics. It is worth noting that for the purpose of the deployment of Lyscale Riskgrade Methodology, the term “Fund” has been used throughout to represent the numerical value or amount derived from any type of activities, whether latent or explicit. Fund is therefore synonymous to “Return” as well as to notions such as “Profit” in an accounting setting; Revenues in a fiscal setting; “Capital” in an Investment setting; “Land Ristourne” in a tertiary setting and “Labour Output” in an Industrial Relations setting.

Polygamma

A special function which is given by the (n+1)st derivative of the logarithm of the gamma function (or, depending on the definition, of the factorial ). This is equivalent to the th normal derivative of the logarithmic derivative and, in the former case, to the th normal derivative of the digamma function. The polygamma function can be expressed in terms of Clausen functions for rational arguments and integer indices.

Parabola Directrix

A parabola (plural “parabolas”; Gray 1997, p. 45) is the set of all points in the plane equidistant from a given line (the conic section directrix) and a given point not on the line (the focus). The focal parameter (i.e., the distance between the directrix and focus) is therefore given by, where is the distance from the vertex to the directrix or focus. The surface of revolution obtained by rotating a parabola about its axis of symmetry is called a paraboloid.

Weierstrass Function

The function was published by Weierstrass but, according to lectures and writings by Kronecker and Weierstrass, Riemann seems to have claimed already in 1861 that the function is not differentiable on a set dense in the reals. However, Ullrich (1997) indicates that there is insufficient evidence to decide whether Riemann actually bothered to give a detailed proof for this claim. Du Bois-Reymond (1875) stated without proof that every interval of contains points at which does not have a finite derivative, and Hardy (1916) proved that it does not have a finite derivative at any irrational and some of the rational points. Gerver (1970) and Smith (1972) subsequently proved that has a finite derivative (namely, 1/2) at the set of points where and are integers. Gerver (1971) then proved that is not differentiable at any point of the form or . Together with the result of Hardy that is not differentiable at any irrational value, this completely solved the problem of the differential.

Amazingly, the value of the Weirerstrass Function can be computed exactly for rational numbers.

CLASSIFICATION OF RISK AND EQUIVALENT BURDEN

Classifying risks is a subjective notion where the rules applied are as many as the rulers themselves. Most of the time, risk is classified with a vested interest perspective enabling many practitioners negating on potential claims especially in the fields of the Insurance Industry. LYSCALE RISKGRADE believes that it is imperative to set a global classification of risks according to scientific precision so as to enable practitioners and other stakeholders to resolve many point of contention and discord within the galaxies Risk Economics, Risk Analytics and Risk Management. In doing so, Lyscale Riskgrade has pioneered this groundbreaking risk classification enacted within the Six systems and 29 Platforms contained within LYSCALE RISKGRADE SYSTEM(R).

Regardless how risk is defined, the greatest burden in connection with risk is that some losses will actually occur. Losses are therefore the primary burden of risk and the primary reason why firms and individuals attempt to avoid risk or alleviate its impact. In addition to the losses themselves, risk had other detrimental aspects. The uncertainty as to whether the loss will occur requires the prudent firm or individual to prepare for its possible occurrence. In the absence of insurance, one way this could be done is to accumulate a reserve fund to meet the losses if they do occur. Accumulation of such a reserve fund carries an opportunity cost, for funds must be available at the time of loss and must therefore be held in a highly liquid state. The return of such funds will presumably be less than if they were put to alternate uses. Moreover, the existence of risk may also have a deterrent effect on economic growth and capital accumulation. Progress in the economy is determined to a large extent by the rate of capital accumulation, but the investment of capital involves risk that is distasteful. Investors as a class will incur the risks of a new undertaking only if the return on the investment is sufficiently high to compensate for both the dynamic and static risks. The cost of capital is higher in those situations where the risk is greater, and the consumer must pay the resulting higher cost of the goods and services or they will be forthcoming.

RISK PROTOCOL SETTINGS

Setting the Lyscale Riskgrade System protocols encompasses the deployment of the whole spectrum of all platforms with differing levels of data capture and the definition of each class of Risk Treatment according to the stance of sources available on the Global Market Place. The idea is to amalgamate sources of information and data provision into one single protocol deployment so as to enable an effective streamlining of provenance and destinations. The reliability of the data provision market is then put on stringent testing exercises in order to provide an accurate aggregation of data veracity using sophisticated aggregator engines. Our aggregator engines, all conceptualised, designed and implemented by Lyscale Riskgrade enable us to fine-tune diversified data provision sources and eliminate discrepancies in those data by replacing them with specific aggregated industry, sector or government-driven scientific approximations to reflect reality. One must stress that many National Statistics Organisations provide biased and sometimes utterly dishonest data about their economies, chiefly among developing countries especially in Africa and Asia. When confronted with such unreliable data provision, Lyscale Riskgrade applies them to the series of Aggregator Engines so as to determine the level consistent with Aggregated Data Veracity (ADV).

Cazare Voronet

Undeniably believe that which you said. Your favorite reason appeared to be on the net the simplest thing to be aware of.

I say to you, I definitely get annoyed while

people think about worries that they plainly do not know about.

You managed to hit the nail upon the top and

defined out the whole thing without having side-effects

, people can take a signal. Will probably

be back to get more. Thanks